Date posted: 27th Feb 2026

If you own UK residential property through a company or another “non‑natural person” structure, the Annual Tax on Enveloped Dwellings (ATED) may apply to you.

With the next key deadline falling on 30 April 2026, now is the time to review your position and make sure your reporting is up to date.

What Is ATED?

Annual Tax on Enveloped Dwellings (ATED) is a UK tax charged each year on certain companies and other entities that hold UK residential property.

It generally applies to:

- UK and non‑UK companies that own UK residential property

- Partnerships with at least one corporate partner

- Certain collective investment schemes

The tax is charged on “single‑dwelling interests” in UK residential property valued at more than £500,000 on the relevant valuation date (usually 1 April 2022, or the acquisition date if later).

Who Needs to File an ATED Return?

You may need to file an ATED return (or a relief declaration return) if:

- Your company or other relevant entity owns UK residential property valued at more than £500,000

- The property is held on the first day of the ATED chargeable period (1 April), or it comes into charge during the year (for example, on acquisition or after development)

Even if no ATED is payable because a relief applies, you usually still need to file a return to claim that relief.

Common situations where ATED can apply include:

- Companies holding residential property as an investment or for letting

- Companies holding high‑value residential property as trading stock

- Corporate partners in partnerships that own residential property above £500,000

Key Dates and the 30 April 2026 ATED Deadline

Each ATED “chargeable period” runs from 1 April to 31 March.

For entities that already own a chargeable property on 1 April:

- The filing window opens on 1 April for the year ahead

- The ATED return (or relief declaration) and any tax due must normally be submitted and paid by 30 April of that same year

This means that for the chargeable period from 1 April 2026 to 31 March 2027:

- Companies and other affected entities that own a relevant UK residential property on 1 April 2026 should expect to file their ATED return and pay any tax due by 30 April 2026.

Different time limits can apply if:

- Your property comes into charge during the year (for example, when you acquire it)

- A newly built or converted dwelling comes into existence

In those cases, filing deadlines are typically within a set number of days from acquisition or from the date the property becomes a dwelling.

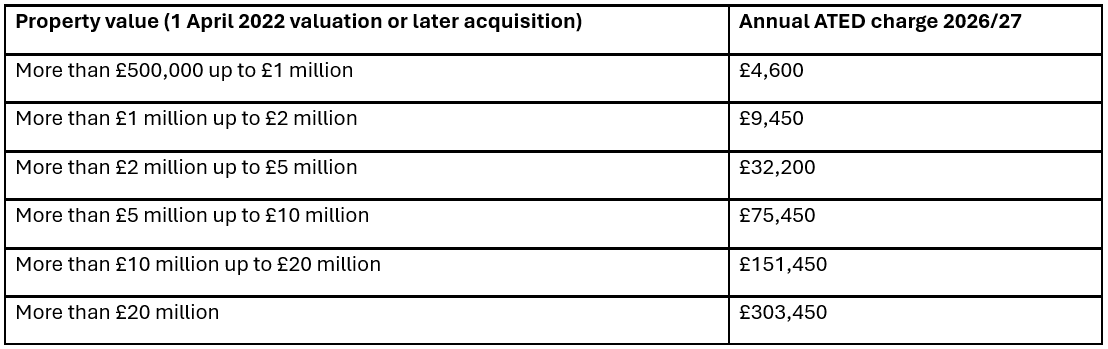

ATED Bands and Charges for 2026/27

ATED is charged according to the value of the property. For the 2026/27 period (1 April 2026 to 31 March 2027), the annual charges are:

These bands are normally increased each year in line with inflation, so it is important to check the latest published figures for the relevant chargeable period.

Missing the 30 April 2026 deadline can result in:

- Late filing penalties

- Interest and penalties on late payment

- Additional scrutiny of your property structures and valuations

Given the values and charges involved, reviewing your position well before 30 April 2026 is essential, especially if:

- Your property value is close to the £500,000 threshold

- You are unsure whether a relief applies

- You have acquired, developed or restructured property recently

If you have any queries regarding ATED reporting, please give us a call.