Date posted: 24th Nov 2022

As the cost-of-living crisis deepens, many employees are looking to save money.

One option is to cut the cost of the commute by cycling to work, which can provide a tax saving.

Exemption for employer-provided cycles

Employees can enjoy the use of employer-provided cycles and cyclists’ safety equipment without having to pay tax on the associated benefit as long as the following conditions are met:

- There is no transfer of property in the cycle or equipment – it remains the property of the employer.

- The employer uses the cycle and/or equipment mainly for qualifying journeys. These are journeys between home and work and business journeys.

- The cycles and/or equipment are made available to the employees who want to make use of them. It is not necessary for each employee to have their own dedicated bike; the employer can operate a pool system where employees who want to borrow a bike can do so from a pool.

Salary sacrifice

A Cycle to Work scheme combines a salary sacrifice arrangement with hire agreement.

Under the scheme, the employee enters into a salary sacrifice scheme and gives up part of his or her salary in return for the provision of a cycle. The employee enters into a hire agreement, under which they hire the cycle from either the employer or a third party. The hire is paid for by the sacrificed salary.

As long as the above conditions are met, the provision of the cycle, by the employer to the employee, is exempt from tax. It is important to stress here that ownership of the cycle must not at this point pass to the employee. As employer provided cycles are protected from the operation of the alternative valuation rules, the exemption is not lost by using a salary sacrifice scheme. The arrangement allows the employee to save tax on the salary given up, and both the employer and employee to save national insurance.

Cycle to work schemes typically run for three years. At the end of the period, the employee has three options:

- Extend the hire agreement.

- Return the cycle and equipment.

- Buy the cycle and equipment.

There are no tax consequences if the employee chooses option 1 or 2. If the employee decides to buy the bike, as long the amount paid is at least equal to the market value of the bike at the time of the transfer, there is no tax to pay. However, if the amount paid is less than the market value, the shortfall is a taxable benefit.

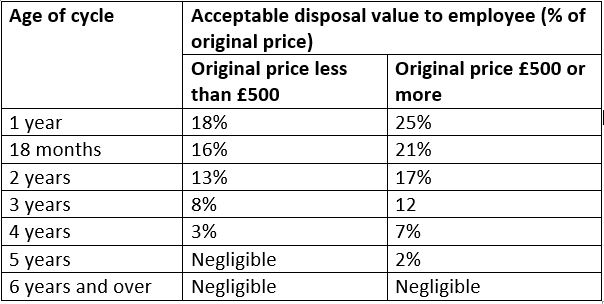

HMRC recognise that it can be difficult to establish the market value of a second-hand bike. Consequently, a simplified approach can be used under which no tax charge will arise as long as the employee pays at least the percentage of the original value for the age and original cost of the bike as shown in the table below.

So, for example, if an employee pays at least £24 for a cycle that originally cost £300 at the end of a 3-year hire period there will be no tax to pay on the transfer, by the employee as they have paid 8% of the £300 original price.

Care needs to be taken, as with all salary sacrifice schemes, to make sure that everyone understands the commercial implications. However, such schemes are common practice and we have helped many clients with tax planning in this area.

If you have any queries regarding the Cycle to Work scheme, please give us a call.