Date posted: 7th Nov 2022

Employers can pay employees a mileage allowance if they use their own car for business journeys.

The Government have recently cleared up confusion as to what can be paid tax-free, confirming the maximum tax-free amount.

Mileage allowance payments

The approved mileage allowance payments system is a simplified system that allows employers to pay tax-free mileage allowance payments to employees who use their cars for business travel. Under the system, payments can be made tax-free up to the ‘approved amount’.

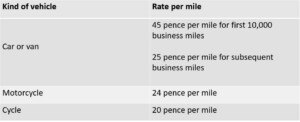

The approved amount

The approved amount for tax is calculated for the tax year as a whole and is simply the reimbursed business mileage for the tax year multiplied by the tax-free mileage rates for the type of vehicle used by the employee. Rates are set for cars and vans, motor cycles and cycles and are as shown in the table below. They have been unchanged for several years now, despite rising fuel costs.

Example

Mo uses his own car for business and drives 12,350 miles in the tax year. The approved amount is £5,087.50 (10,000 miles @ 45p per mile + 2,350 miles @ 25p per mile).

Any payments made in excess of the approved amount are taxable and must be reported to HMRC. If, on the other hand, the employer does not pay a mileage allowance or pays less than the approved amount, the employee can claim a tax deductible expense for the difference between the approved amount and the amount actually paid, if any.

Confusion

Earlier in the year, a petition went before Parliament calling for an increase in the advisory rate from 45 pence per mile to 60 pence per mile to reflect the increases in fuel prices. Parliament rejected the petition stating that the rates remained adequate as they covered all running costs and the fuel element was only a small part. However, in their response, they pointed out that employers could pay higher amounts tax-free where this represented the amount of actual expenditure and could be substantiated:

‘The AMAP rate is advisory. Organisations can choose to reimburse more than the advisory rate, without the recipient being liable for a tax charge, provided that evidence of expenditure is provided.’

The Government subsequently backtracked on this, stating in a written Parliamentary statement that:

‘The response [to the petition] stated that actual expenditure in relation to business mileage could be reimbursed free of Income Tax and National Insurance contributions. This is in fact only possible for volunteer drivers. Where an employer reimburses more than the AMAP rate, Income Tax and National Insurance are due on the difference. The AMAP rate exists to reduce the administrative burden on employers.’

Maximum tax-free amount

The maximum amount that can therefore be paid tax-free to employees using their own car for work is the approved amount, regardless of the car that they drive or the actual costs incurred. However, if the employer wishes to pay more, car sharing could be encouraged and the employer could also pay passenger payments (of 5 pence per mile) for each colleague that the driver gives a lift to (providing the journey is also a business journey for them).

For company car drivers, the maximum tax-free amount that can be paid is governed by the prevailing advisory fuel rates published by HMRC.

If you have any queries regarding tax reliefs for motor expenses or the difference in tax treatments between personally owned cars used for business and company cars, please give us a call.