Date posted: 26th Mar 2026

P11D forms are essential HMRC documents that UK employers use to report taxable benefits and expenses provided to employees and directors. These “benefits in kind” – such as company cars or private medical insurance – must be declared annually to ensure correct tax and National Insurance (NI) charges.

From the 2027/28 tax year, employers must “payroll the benefit,” processing tax directly through payroll instead of filing P11Ds, simplifying compliance for many.

What is a P11D Form?

Employers submit a separate P11D for each employee or director who receives taxable benefits or certain expenses not processed via payroll. A summary P11D(b) form accompanies these to declare total Class 1A NI due from the employer.

- Filed by 6 July following the tax year end (e.g., 6 July 2026 for 2025/26).

- HMRC uses the data to adjust employee tax codes or trigger self-assessment adjustments; employees receive a copy for their records.

- Failure to file on time incurs penalties.

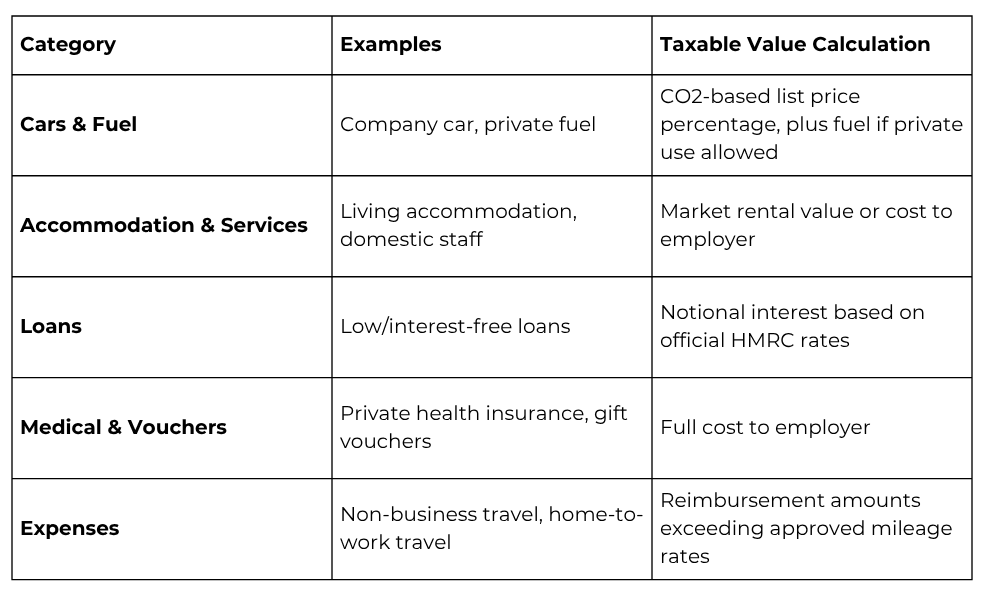

What Does a P11D Report?

P11Ds capture the cash equivalent value of non-cash benefits and non-reimbursed expenses. Common items include:

Class 1A NI (currently 15% on most benefits) is paid by the employer on the total value reported.

Payrolling Benefits: The Major Change from 2027/28

Payrolling benefits – reporting and taxing them real-time via payroll – becomes the default method from 6 April 2027. P11Ds will no longer be required for payrolled items.

Key Benefits of Payrolling

- Real-time tax: Employees see benefits reflected in monthly payslips, with PAYE and NI deducted automatically – no year-end surprises.

- No P11D filing: Reduces admin burden.

- Software integration: Most modern payroll systems (e.g., those HMRC-approved) handle calculations for cars, medical insurance, and other benefits.

Transition Rules

- Employers must notify HMRC via FPS (Full Payment Submission) if payrolling; existing schemes continue seamlessly.

- Optional until 2027/28: You can payroll now or stick with P11Ds, but from 2027/28, non-payrolled benefits stay reportable on P11D (with ongoing filing obligations).

- Cars and fuel remain payrollable; trivial benefits and some exemptions (e.g., pensions) are unaffected.

Employer Actions Now

- Review payroll software for payrolling capability – update if needed.

- Audit current benefits: Identify which can switch (e.g., medical, cars) versus those staying on P11D (e.g., complex loans).

- Train staff: Explain payslip changes to avoid confusion over “higher” taxable pay.

This shift aligns with HMRC’s Making Tax Digital push, prioritising accuracy and reducing end-of-year rushes. For complex setups, professional advice ensures compliance without gaps.

If you need help, we are here to advise.